Menu

Finding the Best Burial Insurance for Your Parents

By Matt Schmidt

Last Updated on June 25, 2026 by Matt Schmidt

2020 has been a scary year so far, to say the least. With the Covid 19 crisis, our world has been turned upside down. Life insurance, especially to address burial costs or final expenses have never been more important to families. While there have been changes to life insurance offerings to the Senior population this year, you can still obtain burial insurance for your parents. We are still here for you and happy to help you out. Call us at 800-470-0179 and let an agent assist you with your insurance needs.

Talking to your parents about burial insurance is a conversation more individuals should be having. It often comes across as uncomfortable and awkward. No one wants to think of a time where their parents are no longer a part of their lives. The reality of not having your biggest fans a part of your life anymore is something everyone can relate to and most individual’s biggest fear comes to life. Sitting down and having those important conversations while they still can will help make that time a little less terrible.

At the end of the day, there’s nothing worse than losing a loved one. And then not knowing how to take care of the funeral expenses to properly bury them.

With the help of a Burial Insurance Pro agent, we can help you with the best policy and price. Put those dreaded conversations to bed by letting us help you find a great agency with little to no hassle. Get back to the finer things in life and enjoy the time you have with your family!

Not knowing where to start the burial insurance process can be frustrating. Don’t let this process be confusing and stressful. Work with one of our agents and have us assist you from start to finish. A quick call to 800-470-0179 is all it takes to speak with a representative.

This is a great question that a lot of people don’t know the answer to. The surprising answer is that you can buy burial insurance for your parents! It’s actually more common than most people think. A lot of children buy burial insurance so they won’t be stuck dealing with all of the final expenses themselves. As much as we don’t like to think about it, one day all of our parents will pass away. Being proactive about burial insurance will allow you to rest assured that when that day comes you’ll have adequate funds and investments to pay for the services needed. These policies will not make a person rich, but rather eliminate the need of using their own funds to cover these funeral expenses.

It’s much easier to invest in burial insurance for seniors now, rather than being hit with massive funeral bills in the future. An ounce of prevention is worth a pound of cure.

These types of plans are actual marketing terms given to smaller amounts of whole life insurance coverage. Burial insurance is the same thing as Final Expense or Funeral Insurance. Many people may only need $3,000 to $50,000 to address their final wishes. Policies are simplified issued. Meaning no medical exams, nor any medical records are needed in order for an underwriting decision to be made.

At the time of death, the listed beneficiary will receive the death benefit in a lump sum, and tax free payment. There are no restrictions on how the money can be used. Some life insurance companies will allow you to assign the policy to a funeral home. This allows the death benefit to be sent to the funeral home directly. Any money leftover is then paid to the beneficiary.

Here are common policy features:

Generally, you will have two types of policies to choose from for your parents

Immediate Death Benefit Policy: This type of policy will pay out an immediate death benefit. No two year waiting period on the full benefit. Popular companies like Mutual of Omaha, Lincoln Heritage, and Sentinel Security may consider your parents for a DAY 1 IMMEDIATE DEATH BENEFIT policy.

Guaranteed Issue Death Benefit Policy: This type of policy is designed to cover people in below average health. If a person dies within 2 years, all premiums paid in, plus 10% interest would be paid to the beneficiary. After 2 years, then full death benefit is paid out at time of death of the insured. Companies like Gerber Life offer these guarantee acceptance policies.

Rates are always going to be determined by the following criteria:

See below for some sample quotes:

| Age | Female - $5,000 | Male - $5,000 | Female - $10,000 | Male - $10,000 |

|---|---|---|---|---|

| 45 | $12.91 | $22.61 | $14.32 | $25.45 |

| 46 | $13.11 | $23.02 | $14.69 | $26.17 |

| 47 | $13.38 | $23.55 | $15.11 | $27.02 |

| 48 | $13.69 | $24.18 | $15.58 | $27.96 |

| 49 | $13.84 | $24.48 | $15.86 | $28.52 |

| 50 | $13.94 | $24.67 | $16.18 | $29.16 |

| 51 | $14.33 | $25.45 | $16.75 | $30.30 |

| 52 | $14.54 | $25.88 | $17.16 | $31.12 |

| 53 | $14.91 | $26.62 | $17.70 | $32.20 |

| 54 | $15.33 | $27.47 | $18.41 | $33.61 |

| 55 | $15.80 | $28.40 | $19.15 | $35.09 |

| 56 | $16.24 | $29.27 | $19.83 | $36.45 |

| 57 | $16.63 | $30.06 | $20.55 | $37.91 |

| 58 | $17.02 | $30.83 | $21.24 | $39.27 |

| 59 | $17.45 | $31.70 | $22.01 | $40.82 |

| 60 | $18.04 | $32.87 | $22.98 | $42.76 |

| 61 | $18.86 | $34.51 | $24.29 | $45.38 |

| 62 | $19.63 | $36.06 | $25.55 | $47.90 |

| 63 | $20.46 | $37.72 | $26.86 | $50.52 |

| 64 | $21.28 | $39.36 | $28.17 | $53.14 |

| 65 | $22.11 | $41.01 | $29.48 | $55.76 |

| 66 | $23.32 | $43.44 | $31.27 | $59.35 |

| 67 | $24.53 | $45.86 | $33.07 | $62.93 |

| 68 | $25.75 | $48.29 | $34.87 | $66.53 |

| 69 | $27.01 | $50.81 | $36.66 | $70.11 |

| 70 | $28.22 | $53.24 | $38.45 | $73.70 |

| 71 | $29.92 | $56.63 | $40.78 | $78.36 |

| 72 | $31.66 | $60.12 | $43.06 | $82.92 |

| 73 | $33.57 | $63.93 | $45.61 | $88.01 |

| 74 | $35.49 | $67.78 | $48.18 | $93.16 |

| 75 | $37.81 | $72.41 | $51.37 | $99.53 |

| 76 | $40.73 | $78.25 | $55.04 | $106.87 |

| 77 | $43.36 | $83.51 | $58.42 | $113.64 |

| 78 | $45.82 | $88.44 | $61.53 | $119.86 |

| 79 | $48.31 | $93.41 | $64.72 | $126.23 |

| 80 | $50.82 | $98.43 | $67.93 | $132.65 |

| 81 | $54.71 | $106.21 | $73.10 | $143.00 |

| 82 | $58.58 | $113.96 | $78.37 | $153.54 |

| 83 | $62.26 | $121.31 | $83.31 | $163.41 |

| 84 | $65.88 | $128.55 | $88.24 | $173.28 |

| 85 | $69.55 | $135.90 | $93.18 | $183.15 |

| 86 | $88.75 | $174.17 | $112.08 | $220.83 |

| 87 | $95.00 | $186.67 | $122.92 | $242.50 |

| 88 | $100.83 | $198.33 | $133.75 | $264.17 |

| 89 | $107.08 | $210.83 | $144.58 | $285.83 |

Buying a burial policy on your parents sounds easy, but you can make mistakes that will come back to haunt you. Afterall, you would hate to purchase a policy, and then not have it pay out when you need it the most.

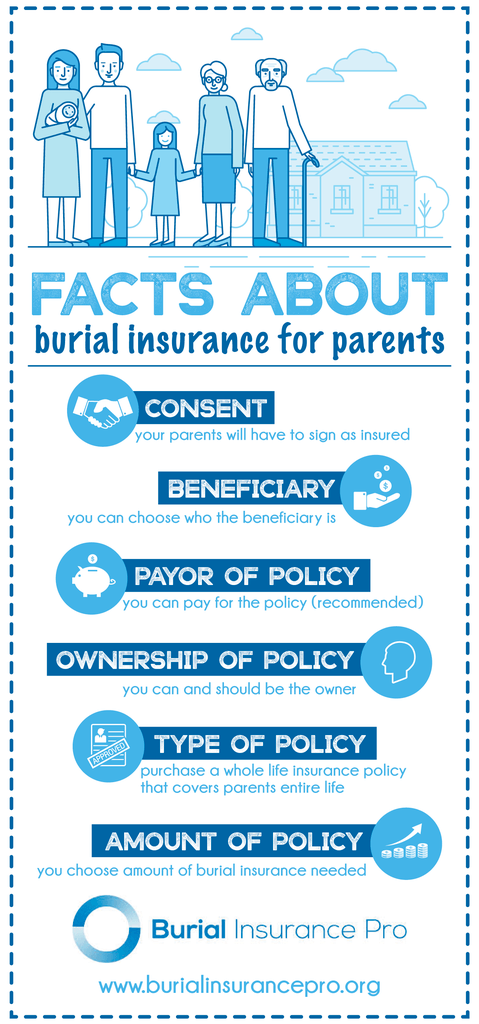

We personally recommend that when setting up the policy, for you, the child, to be the OWNER and PAYOR of the policy if possible. By establishing you as the owner and payor, you will be able to control the policy. Nobody will be able to cancel it, alter it, or stop the payments besides yourself. Being in control of the policy allows you to sleep at night knowing that no sibling or parent is going to cancel a policy without you knowing.

Another important tip is to avoid the Goodman Triangle. According to Insure.com, “A major plus with life insurance is that the death benefit is usually tax-free. Your beneficiaries receive the money and don’t have to worry about a cut going to Uncle Sam.”

But there’s an exception you should know about if you’re planning to buy life insurance and want to protect yourself from a gift tax.

The tax trap is known as the “unholy trinity” or “the Goodman Triangle” after a 1946 court case, Goodman v. Commissioner of the Internal Revenue Service. It happens when three different people play the roles of policy owner, insured and beneficiary.

Think of a life insurance policy as a triangle, says Amy Rose Herrick, a Chartered Financial Consultant and founder of the Money With Amy website. The three points of the triangle are as follows:

How do you avoid Goodman Triangle? Simple. Make sure the Payor and Beneficiary of policy remains the same person.

Just like everything else, when it comes to buying burial insurance there are rules and regulations you must follow to obtain coverage. For the most part, we just want to make you aware of these rules, they very rarely are ever an issue.

Again, we are here to break down this myth. YES! You can get burial insurance for people age 80 or older. Time and time again we find individuals coming to us in need of final expense life insurance. Other companies have told them that it’s too late or that seniors over the age of 80’s can’t receive final expense life insurance due to their age. We are here to let you know, that is not true and we are here to help!

Not only are there tons of burial insurance companies out there that issue to individuals 85 years old or younger but also the coverage they offer goes into effect immediately. As there is no waiting period. As long as they qualify medically, which most applicants do, coverage starts immediately.

Or if your parent is not in the best of health, they could still qualify for guarantee issue burial insurance. Usually, you would have to begin a policy before your parent turns 86. These policies are only needed if there are significant health issues for your parents.

The time is now. Now is the best time to plan on obtaining burial insurance to ensure you or your parent’s final expenses are taken care of and your premiums stay low. Keep in mind that burial insurance will never be cheaper than it is today. The sooner you have it the sooner you’ll appreciate it. Don’t wait until your parent’s age makes the insurance policies, too expensive.

Plain and simple… funerals are expensive. If you were to guess how much the average funeral cost would be, what would you guess–$1,000? $5,000? $10,000? Many people tell themselves that they will save up money in a ‘special’ account that will cover funerals and final expenses. This sounds great on paper. However, in reality, many people will not save properly, and in the event they may leave their family in a ‘bad’ place financially at time of their death.

Next question, do you have that much in your savings that you would be able to borrow from without directly impacting your lifestyle? The average American has less than $5,000 in savings. The average cost of funeral expenses—$8,500. For lots of families, it would make sense to own a burial insurance policy, and know that at the time of their death the policy would pay to their beneficiary.

In 2018, according to the National Funeral Directors Association, the average cost of a funeral was roughly $8,508. A noticeable increase in price from 2014, which was about $6,580. Below will give you a better estimate of some of the costs of a funeral courtesy of the NFDA. Please keep in mind these figures are just estimates of the bare minimum and do not include the cost of cemetery, flowers, obituaries or crematory fees. On average in the last 10 years the cost of a funeral increase roughly 30%.

| Type of Cost | Median Price | Description |

|---|---|---|

| Casket | $2,500 | Cost for a metal casket, your cost will vary based upon the materials you choose. |

| Cremation Casket | $1,200 | A fully combustible container, this can be a traditional casket or cardboard box, but cannot have any metal parts. |

| Cremation Fee | $350 | If the funeral home does not own a crematory and uses a third party. |

| Urn | $295 | Container to hold cremated remains. |

| Required Basic Services Fee | $2,195 | Covers the funeral home’s time, storage of remains and overhead expenses. |

| Embalming | $750 | Not required by law, but a funeral home may require if you hold a viewing. |

| Other Preparation of the Body | $255 | May include cosmetic reconstruction, hair styling and dressing the deceased. |

| Use of Facilities/Staff for Funeral Ceremony | $500 | If you have the ceremony at the funeral home, you can expect to pay this fee. |

| Hearse | $340 | Transporting the remains from the funeral home to the burial site. |

| Service Car/Van | $150 | Transporting the family and guests from the funeral home to the burial site. |

| Printed Materials | $175 | Memorial package and guest book. |

On top of the previously mentioned costs, there are other bills that also need to be considered. Any outstanding bill that has been left by the individual who has passed still needs to be taken care of.

These items, if not accounted for can add up quickly. The best-case scenario is that the policy you purchase is able to cover all of your funeral costs as well as any outstanding bills upon your parents passing.

Being hit with a sudden $7,000-$10,000 bill is not something the average American can take. Signing your parents up for burial life insurance today can help avoid that financial burden and help cushion the blow and burden when that time does finally come.

No one wants to spend the day scouring the Internets for life insurance to cover your parents final life burial costs. It can be extremely frustrating and at times just down right confusing. One site says one thing, while another site almost says exactly the opposite. Where do you even begin? You already did the hard work of talking to your parents. Let us take it from there!

When looking for burial insurance, look for the following criteria.

Like we said before, the best time to get burial insurance is now. With every day that you let pass, the policy that you could have obtained a week ago will be more expensive in price. The sooner you have it, the sooner you will appreciate it.

Keep in mind; everyone’s burial insurance needs are going to be different. When having the conversation with your parents about burial insurance ask them the following questions.

Like we said before, the best time to get burial insurance is now. With every day that you let pass, the policy that you could have obtained a week ago will be more expensive in price. The sooner you have it, the sooner you will appreciate it. Final expense insurance is aged based. The longer you wait to obtain it, the more expensive it will be.

It’s also important to work with an agent who’s knowledgeable about burial insurance. It is extremely important to work with independent burial insurance agent that works with over 15 companies. The agents job will be to help determine what options are available, based off your parents’ health. We are a little biased here, and would encourage you to call us at 800-470-0179.

AARP – First and foremost this type of insurance policy AARP sells does not even include burial insurance. Although they try to push this policy as burial insurance it does not actually include any type of final expense insurance and is incredibly risky to rely on for final burial expenses. Not only that, but it completely expires once your parent turns 80 years old. Unfortunately for the consumer they are hoping you don’t ask too many questions when it comes to this policy. Although a lot of individuals hold AARP as the king for looking out for their best benefit in some cases like burial insurance that is definitely not the case. AARP is in it to make money off of their members, not looking out for their best interests.

Globe Life – Globe Life offers two different types of insurance products. They have whole life burial insurance for individuals who are 0-25 as well as their most popular product being a term life insurance plan. The peculiar thing being that they do not actually offer whole life burial insurance to people over the age of 25.

Globe Life – Globe Life offers two different types of insurance products. They have whole life burial insurance for individuals who are 0-25 as well as their most popular product being a term life insurance plan. The peculiar thing being that they do not actually offer whole life burial insurance to people over the age of 25.

Although their whole life burial insurance for children is actually reasonably priced their programs for seniors misses the mark. Which is why when comparing Globe Life to AARP they show similar deceptive characteristics of falling short with inferior products when it comes to benefiting the customer. Globe Life likes to push this plan on most of their clients. It’s the plan that makes them the most money and is most beneficial to them.

Unfortunately for the client it leaves a lot to be desired for especially since they are giving you a product that doesn’t even last forever. What’s worse is they tend to not be very forthcoming about what their policy actually offers. There are better burial insurance policies out there, compared to Globe Life’s offerings.

Colonial Penn – Is a well-known company with popular marketing campaigns and celebrity endorsement. Their two policies are mostly straightforward to the customer. Neither of the products will expire, both have fixed monthly prices, and the benefits will never decrease. There are, however, two major downfalls to their policies.

Price is expensive when compared against similar products. There are various competitor products which are offered at a lower price. The second drawback is the absence of an independent agent. Colonial Life does not offer a dedicated agent to service you. Instead, a customer service system is used with representatives licensed to sell insurance.

Colonial Penn has some ‘catchy’ commercials, but that does not translate to offering a competitive burial insurance policy. There are better priced options out there.

With technology these days there is very minimal amount of effort when it comes to the application process. For the most part insurance companies will allow for the application to be submitted and signed all within a few emails. We would help you gather the information needed and ask a few health questions and then prepare the application. Once the information is entered into the system you will get an email for review. This allows you to double check that all the information is correct and then off it goes to the insurance company. The decision process takes a few business days and the final policy will be mailed up to 10 business days after that. Quick and easy.

If needed, we can even mail out the forms to your parent’s, for completion and signatures. Ideally, we’d want you to be there to assist. But we do know that may not be possible.

There are a few companies out there that will require you to sign over the phone. That process is just as easy. After answering a few questions you will be able to verbally answer yes or no to sign your application process. A phone signature is very simple, and your agent will assist you, and your parent’s from start to finish.

Enlisting the help of a qualified independent agency, that represents lots of different insurance companies will help you find the perfect fit to your parents health/medical needs. The best part about independent agencies is that they aren’t married to one insurance company, so they will be able to find you the best deal out there!

We have helped many people find the coverage they need at a price that is affordable. We know your options and we help you sort through them – answering any questions you may have along the way. You did the hard part, talk to your parents. Let us help you rest assured that the rest of their burial insurances needs are taken care of. A quick 5 minute phone call to 800-470-0179 is all it takes.

Having a final expense policy in place on your parents is one of the most important financial moves a person can make. Don’t put it off until it’s too late. Once you have a policy, you’ll truly have peace of mind.

Optimized by Seraphinite Accelerator

Optimized by Seraphinite Accelerator