Best Guaranteed Life Insurance Quotes & Reviews

What’s It All About?

That is the biggest question we often get. A lot of individuals out there this is their best option is buying a guaranteed acceptance policy when answering a few simple health questions will allow them to get a lower price elsewhere. You read that right…not only will you get a lower price but also you no waiting period! Let us help you understand all the facts when it comes to obtaining a guaranteed issue life insurance and you can decide what’s best for you.

There are so many types of life insurance because every person and their needs are different. Finding the right type of life insurance will ultimately help you and your family in the long run. Guaranteed life insurance has no underwriting policies. Since there are no underwriting policies there are no health questions asked, no prescription checks and no MIB evaluations. You are GUARANTEED life insurance regardless any type of preexisting condition you may have.

Figuring out what company offers what is confusing enough. Each company has its own way of marketing for guaranteed life insurance policies as well. When doing your research and you stumble across any of the following phrases you are more than likely looking at guaranteed life insurance policy.

Another thing to keep in mind, no insurance company offers term life insurance plans. Of all the companies out there offering guaranteed life insurance you can always assume they are whole life insurance plans.

Term Life Insurance:

A type of life insurance that you get temporarily. You can either have it until a certain age or for a certain amount of years and is single handedly the least expensive type of life insurance on the market.

When your coverage reaches the predetermined age or acquired years your coverage is terminated. Everything you have invested into the term coverage will not be returned. The worst part of this type of insurance, depending on your age you may not be eligible for another term policy. You would have to take out a permanent coverage policy that will be extremely expensive.

Whole Life Insurance:

You gain coverage that will last for as long as you pay your monthly premiums. The downfall of whole life insurance is it is the most expensive type of life insurance. As you make payments over the years to a whole life policy it builds cash value that you are able to borrow from down the line. The more you put in, the more you get out at the end.

What is nice about whole life insurance policies is you can access it for emergencies or to pay your premiums. Although it is not a common practice, if you get behind on your premiums or run into a situation where you need a significant amount of money you are able to take a loan from your policy. The insurance company expects you to pay back your loan in full with interest. If for some reason or another you are unable to pay said loan back, it will be deduced from your final benefit pay out.

Guaranteed Life Insurance – The Waiting Period

When an insurance company gives you a policy with no questions asked there is always a catch. This is that catch. Every company that offers a no questions asked policy would always have a 2-3 year waiting period with no death benefits. If you pass away during that time period you would not receive a death benefit payout. You will be reimbursed for the amount you paid for your premiums during that time period. Once that time period has passed you are fully protected.

The exception to this rule is if your death is ruled an accident. Even if your accident happens during that waiting period your death benefit will be paid out in full.

Keep in mind when doing your research that there is a lot of misleading information out there. No guaranteed life policy will ever pay any portion of a death benefit to you during the waiting period. The only exception is if it is rule an accidental death. If you find anything that states anything other than the information we just provided, it is not accurate.

Guaranteed Life Insurance – The Bottom Dollar

It is expensive to obtain guaranteed life insurance, plain and simple. Since there are no health questions being asked, these types of policies attract a lot of individuals who are in poor health. Due to these high-risk individuals, insurance companies have to make sure they aren’t going to lose out in the grand scheme of things. They will mitigate their risk by offering coverage in small amounts usually no more than $25,000 in coverage.

The truth of the matter is, why pay so much when the majority of individuals who are in search for a policy can find a better option by finding a final expense policy that has underwriting! Qualifying for a plan with underwriting will result in two HUGE benefits.

- You obtain a policy that fully protects you starting on day one of your policy. No 2-3 year waiting period!

- Your monthly payments will be substantially less. Because you are qualifying with your health, the insurance company is taking on less risk which means they can charge less for the insurance.

A final expense life insurance policy that has underwriting is merely one where the insurance company assesses your health. They don’t require physical or medical exams. What they will do is ask you some questions about your health, and check your medication history.

Is It A Good Fit?

The life insurance company is an extremely competitive industry. The biggest thing we try to help individuals understand what it comes to insurance companies is that the primarily compete in two ways.

Price Underwriting

Is the risk worth the reward? The reward being your business! Don’t just assume that you wouldn’t qualify when there are tons of companies out there that will be more than happy to accept your business regardless of your preexisting conditions. If you are able to qualify for a life insurance policy that has underwriting, we would suggest going that route. It will be significantly cheaper for you. Guaranteed life insurance is the most expensive type of insurance out there.

So when is guaranteed life insurance a good fit? Guaranteed life insurance is the perfect fit for individuals who fall under one of these three categories.

If you find yourself nodding your head in agreement with any of the above stated scenarios then maybe guaranteed life insurance is your best option.

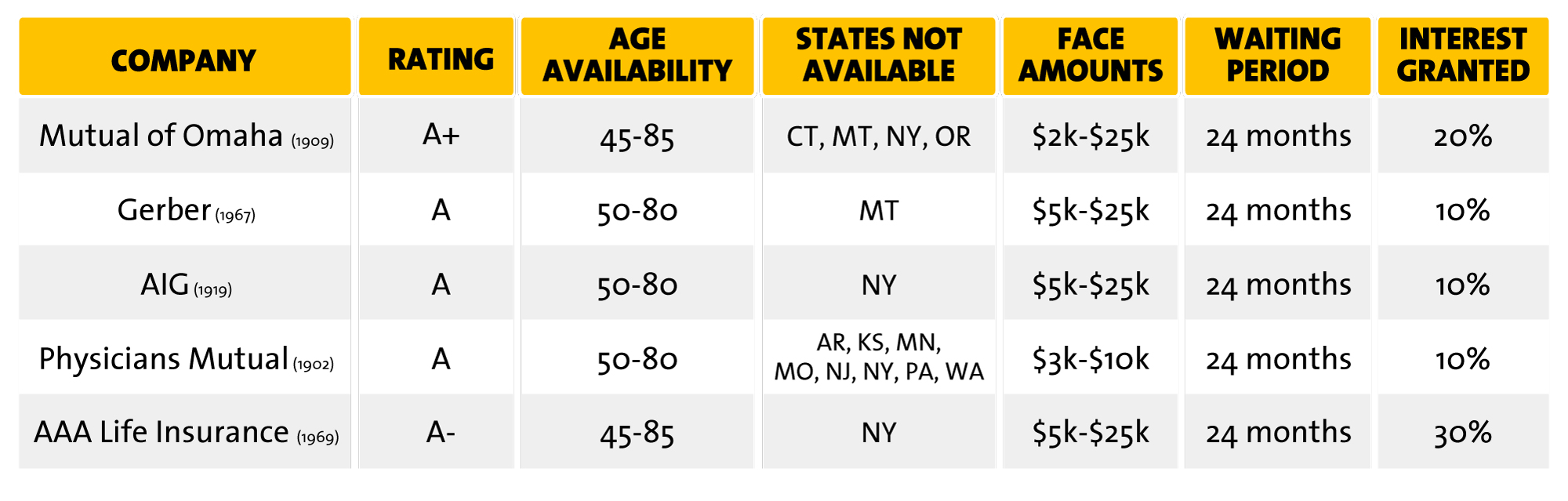

The Top Guaranteed Issue Life Insurance Companies

If you decide that guaranteed issue life insurance is your best bet here is a list of the top companies who offer the best policies with a quick snapshot to help you narrow down your options.

Let Us Help!

We have helped many people find the coverage they need at a price that is affordable. We know your options and we help you sort through them – answering any questions you may have along the way. You are not in this alone

Keep in mind, buying through an agency does not mean you’re going to be paying more. Regardless of which medium you use to purchase your insurance, the law mandates that all insurance prices must be equal.

If you want an experts opinion, fill out the quote form or give us a call to help you out in all of your burial needs!