Foresters Financial Burial Insurance Review for 2026

Last Updated on July 15, 2026 by Matt Schmidt

Foresters Burial Insurance

Foresters Burial Insurance

If you haven’t heard of Foresters Financial, they are one of the top tiered carriers of burial insurance companies. Without investing in any type of marketing they are easily one of the top five biggest insurers in the United States.

The following article will cover Foresters Financial from top to bottom. The unique thing about Foresters is the fact that they offer more than just burial insurance. Foresters also offer their clients with mutual funds, annuities, financial advisory services and retirement savings plans for both business and individuals. Today however this article will primarily cover their insurance programs and hopefully give you all the information you could possibly need to draw an educated answer of whether or not this type of insurance is right for you.

Foresters Burial Insurance – Who are they?

Foresters is an international financial service provider with a unique history that began in 1874 when they set out to provide access to life insurance for average, working families. Their main headquarters is located in Ontario Canada but they operate across every stay within the U.S. as well as Canada & the United Kingdom. Over the years Foresters has also made a name for themselves collaborating with many well-respected professional partnerships. Below are just a few companies Foresters work with to help positively impact the lives of their members and communities.

Something unique is that Foresters is a fraternal benefit society:

A body corporate, without share capital, operating for the benefit of its members and not for profit, with a representative form of government including a lodge system, and that is incorporated for fraternal, benevolent, or religious purposes, including the provision of insurance or annuity benefits to its members, their spouses, children or beneficiaries.

What that means is they have no shareholders. Which to break it down a little more they are considered a not for profit. Anything that they make, that would be considered a profit, goes directly to fulfilling their mission.

The biggest concern individuals tend to have with a fraternal benefit society is that they need to remain solvent by their own accord. What that means is that since they have no guaranteed government backed bailout like other insurance companies, they just need to make sure they are able to pay off any of the insurance certificates they are offering their members. However the likelihood of Foresters every being insolvent would be extremely rare. In our opinion if you want to live risky, take your business elsewhere. Foresters is as close to a safe bet as one can get. Which is why they have been graded with an A rating for the last 15 years.

As Foresters began to grow, so did their products and services offered. As a policyholder you are offered many different member benefits that come at no additional cost including but not limited to burial insurance.

Foresters Benefits

Foresters have one of the most competitive programs out on the market. From being a fraternal benefit society they are able to provide more than just life insurance. Some of the benefits that Foresters offer include:

- Competitive Scholarships – providing over two million dollars in scholarships

- Orphan Scholarships – scholarships provided to children of deceased members

- Emergency Assistance Program – providing short term financial assistance

- Foresters Granting Program – providing grants for volunteering and family activies

- Everyday Money – a hotline that will help you manage your finances

- The Legal Link – providing discounted legal services

- Orphan Benefits – providing monthly stipends to orphans

- Fun Family Events – providing tickets to local entertainment

The best part, all of these “extra” services don’t cost you extra! These type of additional services are what really make Foresters stand out from the rest of their competitors.

Foresters Burial Insurance

When it comes to their burial insurance there are 3 primary options that vary depending on your health status but are all very competitive.

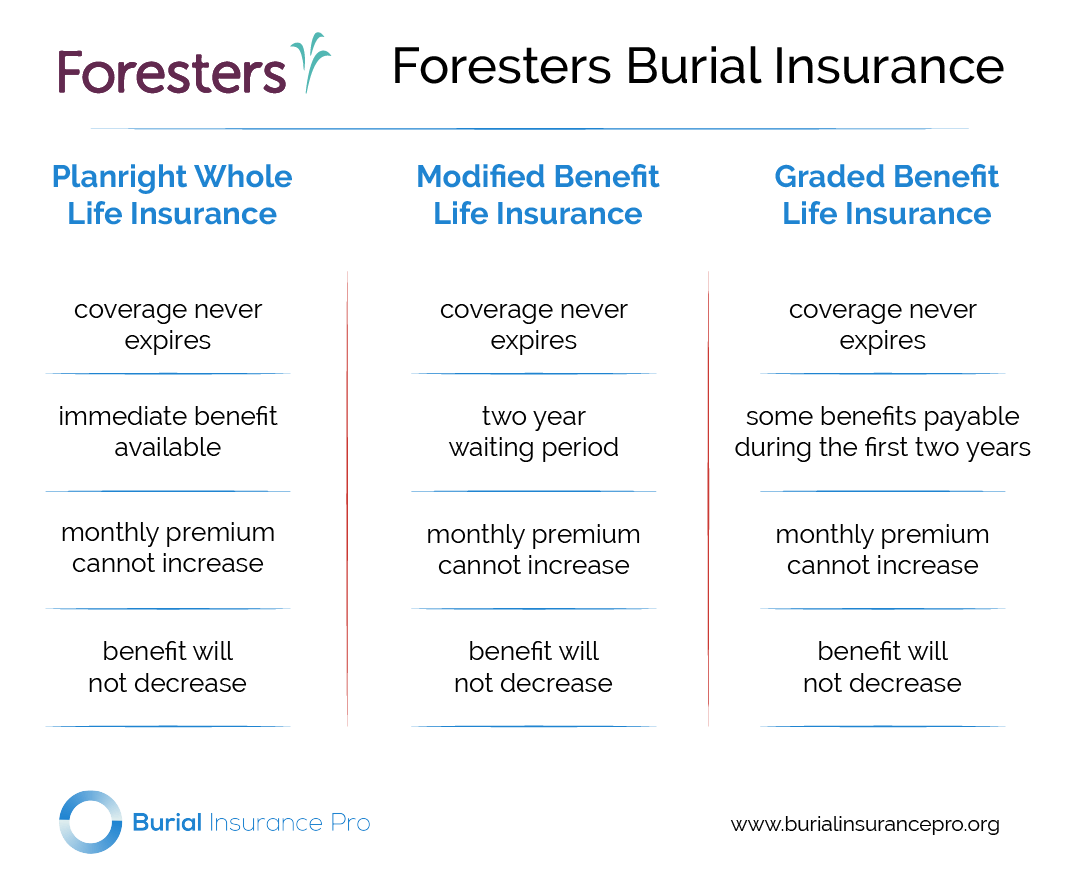

– Foresters PlanRight Whole Life Insurance

This product is Foresters burial insurance that is considered a whole life product specifically for final expenses. It’s a one stop shop in terms of burial insurance and honestly their best option. With the PlanRight program your coverage never expires, you are able to have immediate benefits, your monthly premiums cannot increase and your benefit is guaranteed to no decrease as well. On top of that, the policy comes with a common carrier accidental death ride for no additional charge! One must of course meet the following criteria to be eligible:

- is being operated by a business organized and licensed to transport fare-paying passengers

- is being piloted, driven or captained by a person who is then licensed to pilot, drive or captain that vehicle, to transport fare-paying passengers

- is transporting fare-paying passengers on regularly scheduled routes, from one location to arrive and exit at a different location

If these parameters are met the death benefit would double the previous normal death benefit. Say you were covered for $10,000 and passed away in a helicopter crash, Foresters would pay your normal death benefit of $10,000, and another $20,000 for the common carrier death benefit.

Another amazing benefit that you will receive is their terminal loan option, again at no additional cost. If you become terminally ill Foresters will provide an interest free loan for up to 75% of the total amount if life insurance on your policy, maxing out at $250,000.

The best part of this policy is the fact that it can be achieved within minutes of having your sale interview. After answering Foresters health application questionnaire you will either be covered immediately or denied coverage. The questionnaire has a total of 3 sections; a knockout section, modified section and graded section. Luckily the graded section is nothing you can study for. The following questions are what will be asked of you in the knockout section. If any your answers are yes to the following questions, you will be denied coverage.

- Are you currently: a resident in a nursing home or skilled nursing facility; a patient in a hospital or psychiatric facility; receiving, or have been advised to receive, skilled nursing care, hospice care, or home healthcare; confined to a correctional facility?

- Do you require a wheelchair due to a chronic illness or disease, or do you require assistance (from anyone) with activities of daily living such as taking medications, bathing, dressing, eating, or toileting?

- Within the past 12 months, have you:

- Used, or been advised to use, oxygen equipment to assist with breathing (excluding use for sleep apnea) or had, or been advised to have, kidney dialysis?

- Been advised to have surgery, hospitalization or a diagnostic test (excluding tests related to the Human Immunodeficiency Virus (HIV)) which has not yet been started, completed, or for which results are not known?

- Have you ever received, or been advised to receive, an organ or bone marrow transplant, or had an amputation due to complications of diabetes?

- Have you ever been diagnosed with, or received or been advised to receive treatment or medication for:

- Amyotrophic Lateral Sclerosis (ALS), congestive heart failure, or any terminal illness or end-stage disease?

- Acquired Immune Deficiency Syndrome (AIDS), AIDS Related Complex (ARC), or tested positive for Human Immunodeficiency Virus (HIV)?

- Alzheimer’s disease or dementia, or been prescribed: Aricept, Cognex, Donepezil, Exelon, Razadyne, or Namenda?

- Have you ever had or been diagnosed with more than one occurrence of the same or different type of cancer; or do you currently have cancer (excluding basal cell skin cancer)?

Upon answering no to all of the above questions you will be to continue on to the modified section of your questionnaire. Here Foresters will help determine what type of insurance will be best for you. Keep in mind you can still be declined in these last sections. How you may ask? If something comes up in your prescription history that was consistent with a medical condition asked in your knockout section you could be denied. Don’t worry though; even if you get denied there are tons of other options you can go over with your agent to still achieve a policy to best fit your needs

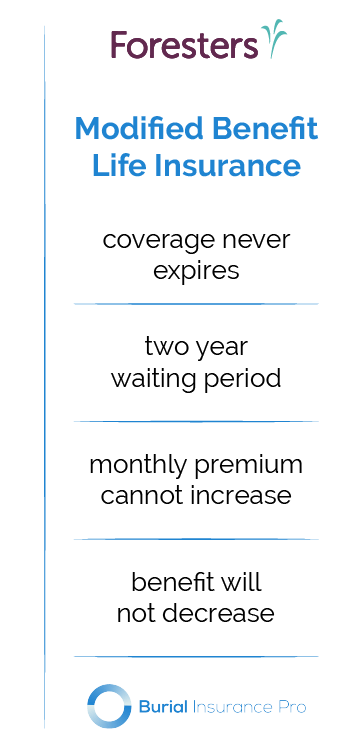

-Foresters Modified Benefit Life Insurance

With the Modified Benefit program your coverage also never expires, your monthly premiums cannot increase and your benefit is guaranteed to not decrease. However with this option, there is a two-year waiting period. To be eligible for this program you still have to say no to all of the knockout health questions from the PlanRight program on top of answering yes to one of the following questions:

- Within the past 2 years have you had, or been diagnosed with, or received or been advised to receive

treatment for medication for:- Alcohol or drug abuse, or have you used illegal drugs?

- Complications of diabetes such as: diabetic coma, insulin shock, retinopathy (eye), nephropathy (kidney), or neuropathy (nerve, circulatory)?

- Within the past 2 years have you had, or been diagnosed with:

- Angina (chest pain), heart attack, cardiomyopathy, or any type of heart or circulatory surgery?

- Stroke or Transient Ischemic Attack (TIA/mini-stroke)?

- Brain tumor or aneurysm?

- Within the past 3 years have you had or been diagnosed with cancer, or received or been advised to receive

chemotherapy or radiation for cancer (the term “cancer” excludes basal cell skin cancer)?

The downfall with this policy is that because it is a modified benefit it costs more and there is a two-year waiting period. If within those first two years you would become deceased, Foresters would not pay out your death benefit. Small plus side being, if you do in fact die within those first two years Foresters will give you back all of the premiums you have ever paid them and an additional 10%. The only way to bypass this rule is if within the first two years your death was considered accidental, then Foresters will pay out the full benefit.

The biggest issue with this policy comes down to the price. Based on the market and other burial insurances offered Foresters modified death benefit is extremely high. In the long run it would be silly to pay more for the same thing offered with a guaranteed acceptance policy. Lucky for you, we can help you find something that would better fit your needs.

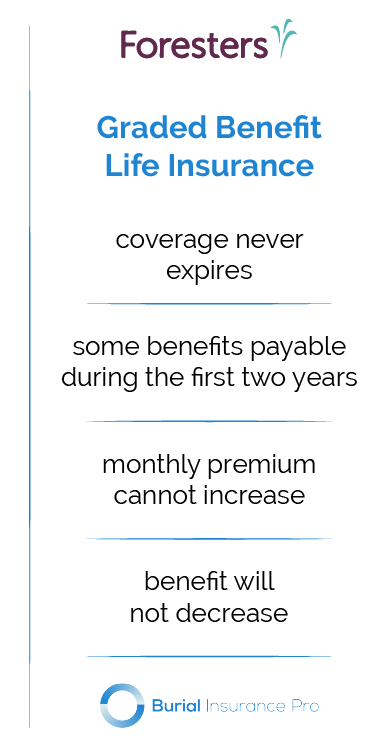

– Foresters Graded Benefit Life Insurance

– Foresters Graded Benefit Life Insurance

To qualify for this plan you would have had to say no to all of the knockout health questions and no to all of the health questions in the modified section. Nearly all of the questions asked are related to chronic illnesses, the most common being COPD. If you answer yes to the following questions you will also be approved:

- Have you ever in your life had, or been diagnosed with, or received or been advised to receive treatment or medication for:

- Parkinson’s disease or Systemic Lupus (SLE)?

- Liver or kidney disease or condition (such as chronic hepatitis or cirrhosis of the liver)?

- Chronic Obstructive Pulmonary Disease (COPD), chronic bronchitis, or emphysema?

This benefit also costs a bit more than the previously stated benefits but is priced similarly to other carriers. As for the payout you will receive a sum greater than all of the premiums you have with a 4.5% interest or 30% of the face amount for the first year and 70% of the face amount for the second year. Once you reach that second year mark you will be guaranteed 100% payout. Similar to the Modified Benefit program, if your death is considered accidental, then Foresters will pay out the full benefit. Luckily for you we can discuss the best option for you and your medical needs.

– Foresters Level Benefit Final Expense

If during the medical questionnaire you are able to answer no to every single health question and clear the prescription history check then you will be able to qualify for Foresters Level Benefit Final Expense policy. This plan is one of the strongest plans they have to offer. The coverage never expires, you receive full coverage immediately, the monthly premium cannot increase and the benefit will not decrease. Upon analyzing the competitions pricing this policy is extremely strong. If you are able to get approved for this type of policy you are one of the lucky ones and beat out other competitors from AARP and Colonial Penn’s price point.

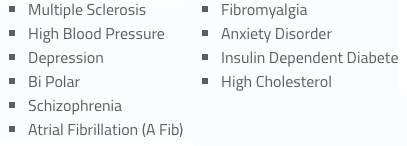

The best part of this type of policy from Foresters is that they accept the following conditions that a lot of other companies would deny coverage:

Final Statements

Final Statements

We hope this review for Foresters burial insurance has helped you understand a little better into what they have to offer as well as their limitations when it comes to their policies. We have had a wonderful partnership with Foresters for many years now and are able to help you find the best policy for you at an extremely competitive price. Not to mention all of the additional member benefits!

If you’re looking for burial insurance that is the best for you and most cost effective, look no further. Our focus here at Burial Insurance Pro’s is burial insurance. That’s what we do and what we excel in. The years of experience we have with our clients allows us the knowledge to know which insurer would suit your needs the best.

If you want an experts opinion, fill out the quote form or give us a call to help you out in all of your burial needs!